Article Highlights:

- Rough Year for the Stock Market

- Year End Approaching

- Annual Capital Losses Are Limited

- Be Aware of Wash Sale Rules

- Off-Set Short-Term Gains with Long-Term Capital Losses

- Planning for Zero Tax on Long-Term Capital Gains

- Converting a Traditional IRA to a Roth

It’s been a rough fall for the stock market. So much so that you should probably carefully review your portfolio and other capital transactions to minimize gain or maximize losses for the year. Remember, capital gains and losses are not just limited to stock transactions. For example, stock losses can offset the gain from the sale of a rental. So you may want to consider other capital transactions you’ve already made this year or could make before the end of the year that would result in a gain that can be offset with stock losses. There can be any number of scenarios that might benefit from year-end planning.

Any transaction you plan must be completed by the end of the year, which is right at the conclusion of the Holidays. Thus, it is probably appropriate to have your planning strategies in place well in advance of the Holidays.

But first here’s a review of the various tax rules and strategies that apply during this severely down stock market.

Annual Capital Losses Are Limited

When planning losses from selling stock, if you have losses remaining after netting losses against capital gains, you can only claim a maximum of $3,000 ($1,500 if filing as married separate) to shelter 2022 ordinary income from salaries, bonuses, self-employment income, interest income, royalties, and other sources. Any excess after the $3,000 ($1,500) is carried over indefinitely until used up to offset capital gains in future years.

Be Aware of the Wash Sale Rules

Some individuals may want to take a loss on a specific stock that’s under water while still maintaining a position in the stock by selling the stock and immediately repurchasing it. Unfortunately, that strategy will not work because of the “wash sale” rules. A wash sale is a sale or other disposition of stock or securities, resulting in a loss, in which the seller, within a 61-day period (which begins 30 days before and ends 30 days after the date of the sale or disposition), replaces the stock or securities by acquiring (by way of purchase or exchange on which the full gain or loss is recognized for tax purposes), or entering a contract or option to acquire, substantially identical stock or securities. The tax law says that a loss on a stock sale that meets this definition is not deductible.

The amount of any disallowed loss will be added to the basis of the repurchased securities. The rule was developed to prevent investors from creating a deductible loss without any market risk.

Off-Set Short-Term Gains with Long-Term Capital Losses

Short-term capital gains do not receive benefits of the special tax rates afforded long-term capital gains. Long-term capital losses, if used to offset long-term capital gains, reduce a gain that would be taxed at no more than 20%. The problem:

ST capital gains are taxed at regular rates.

LT capital losses if used to offset LTCG reduce 10% or 15% income.

Therefore, taxpayers achieve a better overall tax benefit if they can arrange their transactions to offset short-term capital gains with long-term capital losses. Although this cannot always be achieved considering investment strategies, when implemented, it will offset income that would otherwise be taxed at ordinary rates.

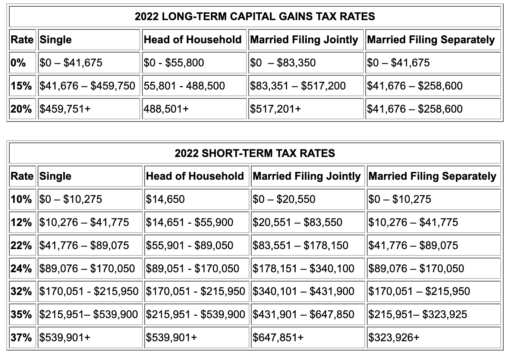

Planning for Zero Tax on Long-Term Capital Gains

Lower-income taxpayers and those whose income is abnormally low for the year can enjoy a long-term capital gain tax rate of zero, which provides an interesting strategy for these individuals.

Even if the taxpayer wishes to hold on to a stock because it is performing well, they can sell it and immediately buy it back, allowing them to include the current accumulated gain in the sale-year’s return with no tax while also reducing the amount of taxable gain in the future. Since the sale results in a gain, the wash sale rule doesn’t apply.

To determine if you can take advantage of this tax-saving opportunity, you must determine if your taxable income will be below the point where the 15% capital gains tax rate begins – see table below.

Example: Suppose a married couple is filing jointly and has projected taxable income for 2022 of $50,000. From the table below we find that the 15% capital gains tax bracket threshold for married joint filers is $83,351. That means they could add $33,350 ($83,350- $50,000) of long-term capital gains to their income and pay zero tax on the capital gains.

Of course, this strategy must be worked out based upon your projected taxable income for the year, which could end up actually being more or less than the estimated amount.

In addition, if you have any loser stocks in your portfolio, you can sell them for a loss, and thereby allow additional long-term capital gains to take advantage of the zero-tax rate.

There are some situations where the increase in adjusted gross income because of the added long-term capital gains could have unanticipated adverse effects that could reduce the overall benefit of this strategy for you. They include reducing any ACA premium tax credit you’d have, and if you are a senior, causing an increase in the Medicare premium withheld from your Social Security benefits.

Tax Rates

Capital gains vary depending on how long an investor had owned the asset before selling it. Long-term capital gains come from assets held for over a year. Short-term capital gains come from assets held for one year or less.

Converting a Traditional IRA to a Roth IRA

Because the stock market is depressed the value of your traditional IRA may also be depressed, if your IRA is invested in stocks or mutual funds, and it may cost you substantially less tax to convert it to a Roth IRA this year, presenting an opportune time for a conversion.

Give this office a call if we can help with your year-end capital gains planning.