Article Highlights

- New Business

- Legal and professional fees

- Spousal Joint Ventures

- Self-employed Health Insurance

- Home Office

- Deducting the Cost of Business Equipment

- Advertising Expenses

- Website Costs

- Financing

- Vehicle Expenses

- Business Meals

As a small business owner, you should always be on the lookout for legitimate ways to minimize your taxes. Waiting for year-end to do your tax planning can be too late and you may miss many possible opportunities. The following are valuable tips that help you maximize your business deductions.

New Business

Normally the costs of starting a business must be amortized (deducted) over 15 years. But taxpayers can elect to deduct up to $5,000 of start-up expenses and $5,000 of organizational expenses on the return for the first year of the business. A qualifying start-up cost is one that would be deductible if it were paid or incurred to operate an existing active business in the same field as the new business, and the cost is paid or incurred before the day the active trade or business begins.

Examples of qualified start-up costs include:

- Surveys/analyses of potential markets, labor supply, products, transportation facilities, etc.;

- Wages paid to employees, and their instructors, while they are being trained;

- Advertisements related to opening the business;

- Fees and salaries paid to consultants or others for professional services; and

- Travel and related costs to secure prospective customers, distributors and suppliers.

Each of the $5,000 amounts is reduced by the amount by which the total start-up expenses or organizational expenses exceeds $50,000. Expenses not deductible in the first year of the business must be amortized over 15 years.

Legal and Professional Fees

incurred in setting up the business would fall under the organizational expense first year deduction of $5,000 and the balance would be amortized over 15 years. However, legal, and professional fees incurred after the business is up and running can be expensed.

Spousal Joint Ventures

When both spouses in a married couple are involved in the operation of an unincorporated business, it is common – but incorrect – for all that business’s income to be reported as one spouse’s income as a sole proprietorship on IRS Schedule C. In which case, the spouse not filing a Schedule C loses out on the chance to accumulate his or her own eligibility for Social Security benefits and the ability to fund a retirement account.

In addition, to claim a childcare credit, both spouses on a joint return must have earned income (or imputed income if one of the spouses is a full-time student or is disabled), so unless the non-Schedule C spouse has another source of earned income, the couple will not be allowed a childcare credit.

There are two ways to remedy this situation, either: (1) by establishing a partnership or (2) a joint venture (each spouse files a Schedule C with their share of the income, deductions, and credits).

Self-employed Health Insurance

If you are a self-employed individual, you can deduct 100% (no AGI reduction) of the health insurance premiums without itemizing your deductions. This above-the-line deduction is limited to net profits from self-employment.

Home Office

Small business owners may qualify for a home-office deduction, which will help them save money on their taxes and benefit their bottom line. Taxpayers can generally take this deduction if they use a portion of their home exclusively for their business and on a regular basis. Plus, this deduction is available to both homeowners and renters.

There are actually two methods to determine the amount of a home-office deduction: the actual-expense method and the simplified method.

Actual-Expense Method – The actual-expense method prorates home expenses based on the portion of the home that qualifies as a home office, which is generally based on square footage. Aside from prorated expenses, 100% of directly related costs, such as painting and repair expenses specific to the office, can be deducted. Unlike the simplified method, the business is not limited to 300 square feet.

Simplified Method – The simplified method allows for a deduction equal to $5 per square foot of the home used for business, up to a maximum of 300 square feet, resulting in a maximum simplified deduction of $1,500. A taxpayer may elect to take the simplified method or the actual-expense method (also referred to as the regular method) on an annual basis. Thus, a taxpayer may freely switch between the two methods each year.

Additional office expenses such as utilities, insurance, office maintenance, etc., are not allowed when the simplified method is used. Prorated rent or home interest and taxes are not either, although 100% of home interest and taxes are deductible as non-business expenses if the taxpayer itemizes deductions.

Deducting the Cost of Business Equipment

From time to time, an owner of a small business will purchase equipment, office furnishings, vehicles, computer systems and other items for use in the business. How to deduct the cost for tax purposes is not always an easy decision because there are several options available, and the decision will depend upon whether a big deduction is needed for the acquisition year or more benefit can be obtained by deducting the expense over a number of years using depreciation. The following are the write-off options currently available.

Depreciation

Depreciation is the normal accounting way of writing off business capital purchases by spreading the deduction of the cost over several years. The IRS regulations specify the number of years for the write-off based on established asset categories, and generally for small business purchases the categories include 3-, 5- or 7-year write-offs. The 5-year category includes autos, small trucks, computers, copiers, and certain technological and research equipment, while the 7-year category includes office fixtures, furniture and equipment.

Material & Supply Expensing

IRS regulations allow certain materials and supplies that cost $200 or less, or that have a useful life of less than one year, to be expensed (deducted fully in one year) rather than depreciated.

De Minimis Safe Harbor Expensing

IRS regulations also allow small businesses to expense up to $2,500 of equipment purchases. The limit applies per item or per invoice, providing a substantial leeway in expensing purchases. The $2,500 limit is increased to $5,000 for businesses that have an applicable financial statement, generally large businesses.

Routine Maintenance

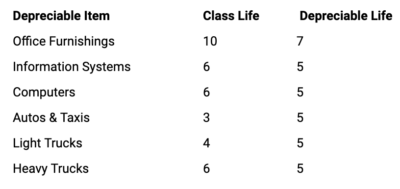

IRS regulations allow a deduction for expenditures used to keep a unit of property in operating condition where a business expects to perform the maintenance twice during the class life of the property. Class life is different than depreciable life.

Bonus Depreciation

The tax code provides for a first-year bonus depreciation that allows a business to deduct 100% of the cost of most new tangible property if it is placed in service during 2022. The remaining cost is deducted over the asset’s depreciable life. This provides a larger first-year depreciation deduction for the item. Bonus depreciation is a temporary provision and for eligible business property bought after 2022, the rates drop to 80% in 2023, 60% in 2024, 40% in 2025, 20% in 2026 and nothing after 2026.

Expensing

Another option provided by the tax code is an expensing provision for small businesses that allows a certain amount of the cost of tangible equipment purchases to be expensed in the year the property is first placed into business service. This tax provision is commonly referred to as Sec. 179 expensing, named after the tax code section that sanctions it. The expensing is limited to an annual inflation adjusted amount, which is $1,080,000 for 2022. To ensure that this provision is limited to small businesses, whenever a business has purchases of property eligible for Sec 179 treatment that exceed the year’s investment limit ($2,700,000 for 2022), the annual expensing allowance is reduced by one dollar for each dollar the investment limit is exceeded.

An undesirable consequence of using Sec. 179 expensing occurs when the item is disposed of before the end of its normal depreciable life. In that case, the difference between normal depreciation and the Sec. 179 deduction is recaptured and added to income in the year of disposition.

Mixing Methods

A mixture of Sec. 179 expensing, bonus depreciation and regular depreciation can be used on a specific item, allowing just about any amount of write-off for the year for that asset.

Advertising Expenses

Once the business is operating, all forms of advertising are generally currently deductible expenses, including promotional materials such as business cards, digital or print advertisements, and other forms of advertising. However any adverting expense incurred before a business begins functioning would be treated as a start-up expense. Trade shows are a form of advertising, and if a business purchases their own custom trade show booth, that booth can generally be expensed in the year purchased using bonus depreciation or Sec 179 expensing.

Website Costs

Although the IRS has not issued guidance on when Internet website costs can be deducted, the costs should generally be treated under the same principles as other business expenses. Generally, website costs will be either a software expense or an advertising expense, but if they are paid or incurred before a business begins, they would be treated as start-up expenses.

Financing

Interest expenses incurred to finance your business operation are deductible as a business expense. But be careful not to mix personal and business interest expenses. Banks are usually reluctant to lend money on a startup business. However, an equity loan on your home will generally achieve a lower interest rate anyway and the interest can be traced to and deductible as business interest.

Vehicle Expenses

If you use your car for business purposes you can deduct its business use by using either the standard mileage method, which allows a per mile amount, or the actual expense method. However, both methods require that you track your business and total mileage for the year. If using the standard mileage method you need to know the number of business miles driven, and if using the actual method you will need to prorate the actual operating expenses including fuel, insurance, repairs, and depreciation by the percentage of business miles to total miles. You can also deduct tolls and parking fees with either method.

Business Meals

Generally business entertainment is not deductible although business meals are 50% deductible, or 100% if the business meals are provided by restaurants during 2021 through 2022. The 100% deductibility provision is to encourage spending at restaurants, which generally were hard-hit by the COVID-19 pandemic emergency lockdowns. Record keeping for business meals is especially important. Each meal expense must be substantiated by not only the amount, date, time, and place, which are usually included on the receipt, but also the business purpose and the names of the guests and their business relationship.

Of course, the list of potential expenses goes on and is too extensive to include all possibilities here. If you are just starting a business or are already in business and have questions related to the business, please give this office a call.