Article Highlights:

- Potential medical deductions

- Medical dependents

- Divorced parents

- Medical AGI limitations

A taxpayer is allowed an itemized deduction for medical expenses paid during the taxable year and not compensated by insurance or otherwise for medical care of the taxpayer or the taxpayer’s spouse, dependent, or medical dependent.

Alcoholism and drug addiction are treated as medical ailments for tax purposes. People with addictions often cannot quit on their own; addiction is an illness that requires treatment. Generally, treatment expenses are tax deductible as itemized deduction medical expenses. Possible deductible expenses include the costs of:

- Doctors

- Prescribed medications

- Laboratory testing

- Psychological services

- Treatment programs

- Inpatient treatment at a therapeutic center for alcoholism or drug abuse, including meals and lodging furnished as necessary incident to the treatment

- Counseling

- Behavioral therapies

To claim these expenses for someone other than the taxpayer, the person must have been the taxpayer’s dependent or spouse either at the time that the medical services were provided or at the time that the expenses were paid.

Medical Dependent

Tax law does include a special provision that allows medical expenses to be deducted for an individual who does not meet all the requirements to qualify as a dependent. A person generally qualifies as a “medical” dependent for purposes of the medical expense itemized deduction if:

- That person lived with the taxpayer for the entire year as a member of the household (temporary absence to obtain medical treatment is an exception) OR is related to the person,

- That person was a U.S. citizen or resident or a resident of Canada or Mexico for some part of the calendar year in which the tax year began, and

- The taxpayer provided over half of that person’s total support for the calendar year.

The medical expenses of any person who meets these qualifications may be included even if he or she cannot be claimed as a dependent on the taxpayer’s return.

Thus, the dependent’s age and income are not limiting factors in determining whether an individual is a dependent for purposes of deducting their medical expenses.

For example, suppose an adult child has an addiction problem. Even though the child is an adult and generates an income, a parent may still be able to deduct medical expenses that he or she pays for the adult child if the three requirements above are met. The parent must pay the medical service providers directly and not just give the money to the dependent to pay the bills.

In the case of divorced parents, if either parent qualifies to claim a child as a dependent, then each parent can deduct the medical expenses each paid for the child. However, consider the limitations (discussed below) that might preclude any deduction for one of the parents, and plan payments accordingly.

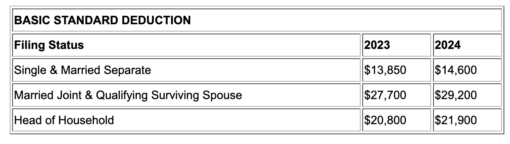

Two situations will prevent a taxpayer from deducting otherwise eligible addiction-related medical expenses. The first is that medical expenses are only allowed as an itemized deduction to the extent that total medical expenses exceed 7.5% of the taxpayer’s adjusted gross income (AGI). The second hurdle is that if the taxpayer’s standard deduction amount is greater than the total of all allowed itemized deductions, there’s no tax benefit to itemizing, and therefore, no medical expenses would be deductible. For 2023 and 2024, the standard deduction amounts are:

A taxpayer, and spouse if married, age 65 and older, or blind, is allowed an additional standard deduction amount:

For 2023: $1,850 for single and head of household status; $1,500 for married (either joint or separate) and qualifying surviving spouse.

For 2024: $1,950 for single and head of household status; $1,550 for married (either joint or separate) and qualifying surviving spouse.

As you can see, these and other tax rules related to medical deductions can become complicated. If you need assistance in planning medical expenditures for maximum tax benefits or determining whether you can deduct certain expenses, please call.