Article Highlights:

- Special Transfer Option

- Does the Vehicle Qualify for Credit

- MSRP and Purchase Price

- Taxpayer Qualifications

- Modified AGI

- Applying for the Credit Transfer

- Change of Mind

- About the Credit

Beginning in 2024, a special election allows a taxpayer purchasing a new clean vehicle or previously owned clean vehicle, to transfer the entirety of the allowable credit to an eligible (registered) dealer. The dealer in turn applies the credit to the purchase of the vehicle. In short, the tax credit can be applied to reduce the cost of the purchase by the amount of the credit. This also make it easier for taxpayers to meet down payment requirements and avoids waiting for the credit until their tax return for the year of purchase is filed.

The dealer will be reimbursed by the federal government for the credit amount that is applied to the purchase.

A buyer choosing to transfer the credit to the dealer is not mandatory, and taxpayers can still choose to claim the tax credit on their return instead of transferring a new or previously owned clean vehicle tax credit to the dealer. However, should a taxpayer choose to transfer the credit to an eligible dealer there are several issues that should be considered before making that decision.

Does The Vehicle Qualify for Credit?

Although a dealer must provide a certification that the particular vehicle qualifies for the credit, someone shopping for credit-qualified vehicles may wish to first determine which vehicles, both new and previously owned, qualify for credit. The following websites will provide that information.

- New vehicles qualifying for credit is provided by The Department of Energy.

- Previously owned clean vehicles qualifying for credit is provided by the IRS.

Qualified vehicles must also have prices below certain caps. For new vehicles, the manufacturer suggested retail prices (MSRP) must be below $80,000 for SUVs, vans, and trucks and $55,000 for others. For a previously owned clean vehicle the dealer price must be $25,000 or less. In addition, a previously owned clean vehicle must be a model year which is at least two years earlier than the calendar year in which the taxpayer acquires it.

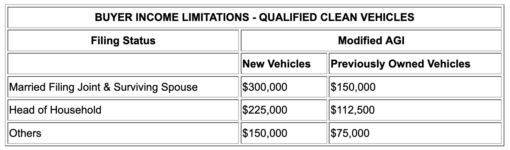

Taxpayer Qualifications

First and foremost, a taxpayer needs to make sure they qualify for a credit. The credit, beginning in 2023, limits the income of the buyer that can qualify for a credit and these limitations are different for new clean vehicles and previously owned clean vehicles. If their modified adjusted gross income (MAGI) is even $1 over the limit, the taxpayer will not qualify for the credit. Taxpayers can use the MAGI from either their 1040 return for the year of purchase or the return for the previous year. Thus, if purchasing a vehicle in 2024, either the 2023 or 2024 MAGI can be used. The MAGI limitations are illustrated in the table below.

MAGI for most taxpayers is the same as AGI which appears on line 11 of the 1040. However, in rare cases, taxpayers may have excluded income from foreign counties or U.S. possessions, and these exclusions must be added back for purposes of the limitations, thus the term modified AGI.

In addition, a taxpayer purchasing a previously owned clean vehicle must not be a dependent of another person, and in the prior 3 years cannot have been allowed a credit for a previously owned clean vehicle.

It is important to note, that should a taxpayer successfully have a credit transferred to an eligible dealer, and not qualify for the credit, then they must repay the credit on the return for the year of purchase. There are no forgiveness provisions. For some taxpayers this could be an unexpected financial hardship.

Applying for the Credit Transfer

The taxpayer must provide the eligible dealer from whom the taxpayer intends to purchase the new or previously owned clean vehicle required information which the dealer will then submit to the IRS for approval. If the sale report is approved by the IRS, it is anticipated the funds will be transferred to the dealer within 48 to 72 hours. Dealers will receive real time online confirmation as to whether an advance request was accepted or rejected. If the seller report is rejected, the taxpayer may not claim the new clean vehicle credit or previously owned clean vehicle credit. Therefore,purchasers and dealers are strongly encouraged to receive confirmation of a successfully submitted seller report before finalizing a sale and placing a vehicle in service.

The purchaser information needed to be submitted includes:

- Date of the transfer election.

- Taxpayer identification number (generally the taxpayer’s Social Security number).

- A photocopy of a valid government-issued photo identification document (such as a driver’s license or passport).

- The following attestations:

- That either MAGI for the prior year OR the current did not exceed the limits. If not known, then to the best of their knowledge it will not exceed the limits.

- For new clean vehicles, that the vehicle will be used predominantly for personal use or for previously owned clean vehicles, that the qualified buyer requirements are met.

- An income tax return will be filed for the taxable year in which the vehicle is placed in service with proof of certain qualifications. o Election is prior to placing the vehicle in service and this is the first or second transfer election made during the taxable year.

- If the MAGI limits are exceeded the advance credit will be repaid for the tax year the vehicle was placed in service. o The credit transfer was voluntarily elected.

Change of Mind

Once the sale is finalized, the taxpayer cannot change their mind about whether to transfer the credit to the dealer.

About the Credit

The clean vehicle credits are non-refundable and there is no carryover. Non-refundable means it can only offset a taxpayer’s tax liability on their tax return for the year claimed and any excess is lost.

In addition, where the taxpayer has the credit transferred to the dealer, the IRS says you can’t transfer a partial credit, it is all or nothing. For a taxpayer in this situation it may be more appropriate to just wait and claim the credit when they file their tax return. In doing so they avoid receiving the full benefit of the credit through the dealer and having to repay a portion. Whereas by claiming the credit on the tax return they only get credit for the amount they are entitled to.

As you can see there is a lot to consider related to the new and previously owned clean vehicle credit. Please contact this office for assistance related to your particular circumstances.