Article Highlights:

- Reason for Conversion

- Basis

- Depreciation

- Cash Flow versus Tax Profit or Loss

- Passive Losses

- Home Gain Exclusion

- Other Tax Issues

- Becoming a Landlord

With the current substantial appreciation in home values and demand for housing exceeding the available inventory, along with low home mortgage interest rates, more and more homeowners are converting their existing homes into rentals when they buy a new home. Other reasons individuals may make the conversion include maximizing the tax benefits for an elderly person who can no longer live alone by delaying the sale of that person’s home; and to ensure that a home provides value when its owner takes a temporary job assignment in a different location. Some homeowners even mistakenly think that, when a home has declined in value, converting it into a rental can allow them to deduct that loss. Regardless of why an individual considers making a conversion, several tax matters come into play when making that decision.

Basis

The basis of the converted property is a good place to start examining these conversion-related tax issues. The basis is the starting value that is used to calculate gains or losses for tax purposes. The basis is also used to determine the amount of depreciation that can be claimed for property used in the rental activity. Generally, for depreciation purposes, a property’s depreciable basis on the date of the conversion is the lower of its adjusted basis (the original cost, plus the costs of any improvements, minus any deducted casualty losses) or its fair market value (FMV).

Example #1: A home’s original purchase cost was $250,000; the homeowner later added a room at a cost of $50,000. At the time of the conversion, there had been no casualty losses, so the home’s adjusted basis is $300,000 ($250,000 + $50,000). By comparison, the property’s FMV is $350,000, so the depreciable basis for the rental is the lower of the two amounts: $300,000.

Example #2: If, on the date of the conversion, a home has the same adjusted basis as in Example #1, but its FMV is only $225,000, then the depreciable basis used for the rental is equal to $225,000, as that is the lower of the two amounts.

When a home’s FMV is less than its adjusted basis on the date of conversion, as in Example #2, the rental has dual bases:

- If the rental is subsequently sold for a loss, the basis for loss is the FMV on the date of the home’s conversion. Because losses from the sale of personal-use properties (such as homes) are not deductible, this rule prevents homeowners whose homes have declined in value from converting them into rentals in order to claim tax losses.

- If the rental home is subsequently sold for a profit, the basis for the gain is the property’s adjusted basis.

Depreciation

Depreciation is an allowance that both accounts for wear and tear and provides a systematic way for the owner to recover the initial investment in the property. This is necessary because tax law doesn’t allow homeowners to deduct the entire cost of a residential rental at one time. Despite this statutory allowance for the depreciation of residential rentals, real properties have historically appreciated rather than depreciated, so this allowance typically provides a significant tax advantage (i.e., a write-off). Here is how to determine the depreciation for a residential rental: First, reduce the basis by the value of the surrounding land (as land is not depreciable) to get the value of the improvements to the home (i.e., the structure); then, multiply that value by .03636 (the annual depreciation rate). In the conversion year, the resulting amount has to be prorated by the number of months used as a rental. Generally, the value of the land is based on a property-tax statement. For example, if a property-tax statement values an entire property at $240,000 and its land at $80,000, then 1/3 of the basis ($80,000 / $240,000) is allocated to land; the remaining 2/3 is allocated to improvements. Thus, if the basis is $300,000, then the depreciable improvements are valued at $200,000 (2/3 × $300,000), and the annual depreciation deduction is $7,272 (.03636 × $200,000).

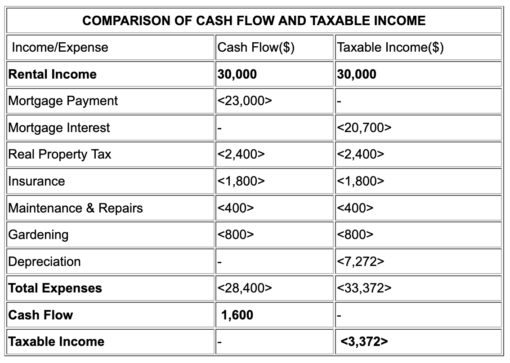

Rental Cash Flow versus Taxable Profit or Loss

Cash flow is the net amount after subtracting expenses from rental income, and the taxable profit or loss is the rental income minus any allowable tax deductions. Of course, higher cash flow is always better, but it is particularly important to avoid having a rental with a negative cash flow. The following example compares cash flow to taxable income.

The major difference between cash flow and taxable income is that cash flow includes the deduction for the entire mortgage payment (not just the interest) but does not include the deduction for depreciation. In the above example, the rental has $1,600 in positive cash flow for the year but also has a passive loss (tax write-off) of $3,372.

Passive Losses

Losses from residential rental real estate are classified as passive and can only offset passive income; deductions from passive losses are also limited to $25,000 per year for most taxpayers with adjusted gross incomes (AGIs) of $100,000 or less. This limit is then ratably phased out for AGIs up to $150,000. Thus, taxpayers’ ability to benefit from a tax write-off on a rental is dependent upon their AGIs. The good news is that the passive losses in excess of this limit carry over to future years and can be used to offset other passive income in those years; in addition, any unused carryforward amount and any passive losses in the sale year are deductible in full once the rental is sold.

Home Gain Exclusion

IRC Section 121 allows homeowners to exclude up to $250,000 of gains from a home sale if they owned and used that home (as their primary residence) for at least 2 of the 5 years prior to the sale date. The amount that can be excluded jumps to $500,000 for married couples who are filing jointly – provided that both have used the property as a primary residence for 2 out of the prior 5 years and at least one has owned the property for 2 out of the prior 5 years. This is a very important consideration because, once a home is converted into a rental, the homeowner(s) will lose the ability to exclude gains after 3 years (because at that point, it is no longer possible to meet the 2-out-of-5-years qualifications).

Even when a homeowner sells a rental property after its conversion but before the exclusion period expires, any depreciation that was claimed during the rental period must be recaptured as taxable income.

Other Tax Considerations

This article has covered only some of the tax issues affecting rental property. Others include the qualified business income deduction available for trade or business owners which generally include landlords, requirements to issue 1099 forms to service providers, and special rules for real estate professionals. If you have a “homeowner’s exemption” on your home for real estate tax purposes, in most jurisdictions when you convert the home to a rental you will no longer be eligible for this exemption, so you should expect to pay higher property taxes.

Being a landlord will come with some problems, such as repairs and maintenance, and of course, making sure you rent to responsible tenants. For those that do not wish to deal with landlord responsibilities, management firms are generally available for a fee, which counts as a rental expense for tax purposes.

The benefits of renting include cash income, tax write-offs, and most of all, long- term appreciation of the property. But not all circumstances warrant converting a home to a rental versus selling it. Please contact this office for assistance with the financial and tax aspects and the pros and cons of converting.