Article Highlights:

- Employer Medical Fringe Benefits.

- Flexible Spending Account (FSA).

- FSA Annual Contribution Limits.

- FSA Limited Annual Carryover Provisions.

- Health Savings Account (HSA).

- HSA Qualifications.

- High Deductible Insurance.

- HSA as a Retirement Vehicle.

- Comparison Table.

Many employers offer health flexible spending accounts (FSAs) and health savings accounts (HSAs) as part of their employee benefits packages. Both plans allow you to set aside money to pay medical expenses with pre-tax dollars, providing a significant tax benefit. But which is the better option?

Although FSAs are only available through an employer, you may be able to open an HSA on your own if you have an HSA-eligible health plan through work, your spouse’s employer, private insurance, or the insurance marketplace.

How Health Flexible Spending Accounts Work

A Health Flexible Spending Account (FSA, also called a “flexible spending arrangement”) is a special account you put money into that you use to pay for certain out-of-pocket health care costs.

You don’t pay taxes on this money. This means you’ll save an amount equal to the taxes you would have paid on the money you set aside. Employers may make contributions to your FSA, but they aren’t required to. With an FSA, you submit a claim to the FSA (through your employer) with proof of the medical expense and a statement that it hasn’t been covered by your plan. Then, you’ll get reimbursed for your costs.

To learn more about FSAs, contact your employer for details about your company’s FSA, including how to sign up.

Facts about Health Flexible Spending Accounts (FSA)

- The amount you can put into an FSA for 2023 is limited to $3,050 per employer. If you’re married, your spouse can put up to $3,050 in an FSA with their employer too. The amount is indexed for inflation each year.

You can use funds in your FSA to pay for certain medical and dental expenses for you, your spouse if you’re married, and your dependents.

- You can spend FSA funds to pay deductibles and copayments, but not for insurance premiums.

- You can spend FSA funds on prescription medications, as well as over-the-counter medicines with a doctor’s prescription. Reimbursements for insulin are allowed without a prescription.

- FSAs may also be used to cover costs of medical equipment like crutches, supplies such as bandages, and diagnostic devices like blood sugar test kits.

- You generally must use the money in an FSA within the plan year. But your employer may offer one of 2 options:

- It can provide a “grace period” of up to 2-½ extra months to use the money in your FSA.

- It can allow you to carry over up to $610 per year (the 2023 inflation adjusted amount) to use in the following year.Your employer doesn’t have to offer these options. If it does, it can be either one of these options.

- Don’t put more money in an FSA than you think you’ll spend within a year on things like copayments, coinsurance, drugs, and other allowed health care costs.

Health Savings Account (HSA)

Is a type of savings account that lets you set aside money on a pre-tax basis to pay for qualified medical expenses. By using untaxed dollars in a Health Savings Account (HSA) to pay for deductibles, copayments, coinsurance, and some other expenses, you may be able to lower your overall health care costs. HSA funds generally may not be used to pay premiums.

While you can use the funds in an HSA at any time to pay for qualified medical expenses, you may contribute to an HSA only if you have a High Deductible Health Plan (HDHP) — generally a health plan (including a Marketplace plan) that only covers preventive services before the deductible. For plan year 2022, the minimum deductible for an HDHP is $1,500 for an individual and $3,000 for a family. When you view plans in the Marketplace, you can see if they’re “HSA-eligible.”

For 2023, if you have an HDHP, you can contribute up to $3,850 for self-only coverage and up to $7,750 for family coverage into an HSA. HSA funds roll over year to year if you don’t spend them. An HSA may earn interest or other earnings, which are not taxable if used for qualified medical expenses. Some health insurance companies offer HSAs for their HDHPs. Check with your company. You can also open an HSA through some banks and other financial institutions.

Establishing and contributing to an HSA can be more than just a way for individuals to save taxes and gain control over their medical care expenditures. It can also be a retirement vehicle, especially for taxpayers who are maxed out on their other retirement plan options or who can’t contribute to an IRA because of the income limitations. There is no requirement that medical expenses must be paid or reimbursed from the HSA, so a taxpayer can maximize tax-free growth in the account by using funds from other sources to pay routine medical costs. Later, distributions can be used tax-free to pay post-retirement medical expenses. Or, if used for non-medical purposes, an individual aged 65 or older will pay income tax, but not a penalty, on the distribution. Unlike IRAs, no minimum distributions are required to be made from HSAs at any specific age.

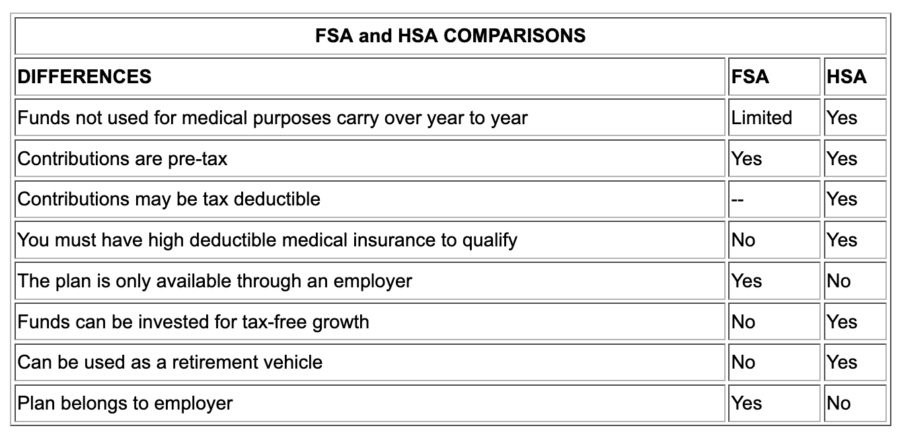

As you can see an HSA allows larger contributions and retirement options but requires high deductible medical insurance to qualify. While an FSA is only available if your employer offers an FSA as an employee benefit, but only has limited carryover of unused funds.

If you have further questions related to HSAs and FSAs, please give this office a call.